SaaSpocalypse or Sorting?

Citrini’s thought experiment isn’t prophecy, but it shows how markets are starting to think.

Citrini’s thought experiment isn’t prophecy, but it shows how markets are starting to think.

Earlier this week, a speculative AI scenario from Citrini Research echoed through the global markets and triggered sell-offs in software stocks. While the report was not an actual forecast, it highlighted the deep anxiety running through the public market i.e. rapid advances in AI could erode pricing power and revenue models of companies built over decades. Importantly, the thesis extended well beyond software, arguing that AI’s acceleration could reshape labor markets, services, and entire economic structures. Even as a thought experiment, it deserves our attention: not as a certainty, but for the questions it raises.

And nowhere are these pressures more visible than in software. The very industry that created digital workflows now finds those workflows exposed to AI and automation.

A seismic shift in software is underway

Just as cloud disrupted legacy infrastructure and rewired who captured value, AI is now changing the economics of software itself. “SaaSpocalypse”, the term coined to define it, refers to the predicted collapse in the business prospects and market valuations of traditional SaaS companies, due to the powerful AI agents that can replace many SaaS tools and workflows. Even software companies with stable cash flows are finding their position challenged by recent launches such as Claude Cowork, Perplexity Compute etc.

But is this the end of SaaS? Is every incumbent software company destined for obsolescence simply because AI agents can now replicate workflows once locked inside applications? That conclusion is as tempting as it is misleading.

Technology shifts rarely erase entire categories uniformly. Cloud did not eliminate software vendors, but it rewired the industry’s cost structure and shifted power toward platforms, while expanding value of the application layer for vendors who embraced scale early. Mobile did not destroy the web, but it redefined distribution and interfaces for companies that relied primarily on browser based access. In each wave, value did not disappear. It reallocated towards companies with structural advantages.

The same will be true of AI. Some software companies will indeed see their pricing power compress as intelligence becomes commoditized. Others will discover that AI enhances, rather than erodes, their business and economic foundation. The difference will lie in the key characteristics of the business.

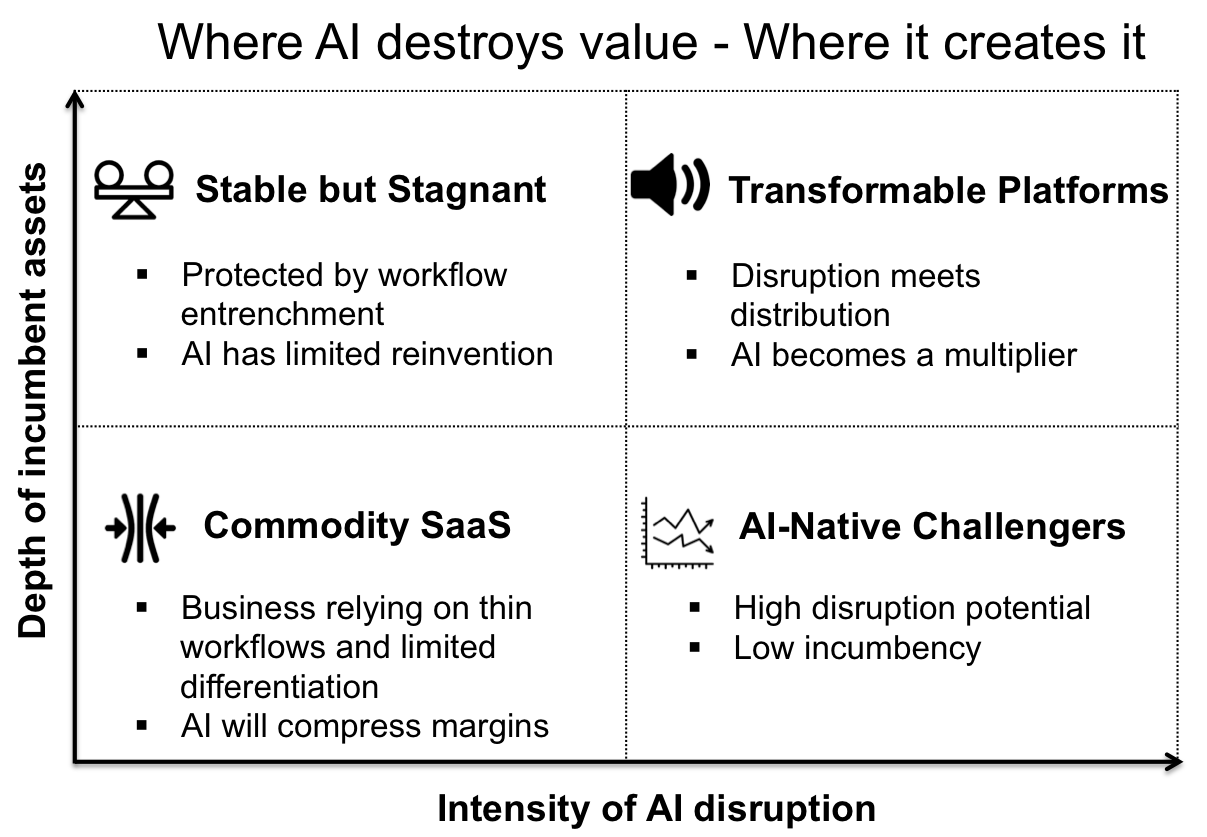

The different futures of software companies in the AI Era

Two forces determine the likely trajectory of a software company in the AI era

1. The intensity of AI disruption in its category: how much AI can fundamentally alter cost structures, user behavior, competitive dynamics.

2. The depth of its incumbent assets: the strength of the proprietary data, workflow entrenchment, distribution, customer trust, integration advantages.

What looks chaotic at the market level resolves into four distinct archetypes.

1. Commodity SaaS: These are the companies most vulnerable in the AI era

Characteristics

- Horizontal tools with narrow workflow

- Low switching costs and minimal integration depth

- Limited proprietary data advantage and minimal integrations at customer deployments

Impact/Risk

- AI can replicate their core functionality, so AI-native companies can recreate their value quickly

- Customers can rebuild similar workflows internally using copilots/agents

Outcome

- These companies will face pricing and margin pressure

Examples

- Email marketing tools and Marketing automation platforms

- Standalone scheduling tools

- Simple CRMs and project management apps

2. Stable but stagnant: Limited AI disruption to the core business

Characteristics

- Deeply embedded in regulated or compliance-heavy workflows

- Mission critical software turns switching costs into operational risk for customers

Impact/Risk

- AI can improve internal company efficiency, but the nature of their products provide limited ability to use AI to impact core value

- Regulatory complexity reduces rapid AI based substitution

Outcome

- AI based improvements via automation

- Limited revenue impact from AI

- Limited possibilities for transformation

Examples

- Payroll software, benefits software

- Tax filing and compliance platforms

- Government workflow software

3. AI-native companies: The disruptors operating in a volatile space

Characteristics

- Born in the AI era with model-first or agent-first architectures and rapid iteration cycles

- No incumbency to protect but untested GTM

Impact/Risk

- Weak distribution and limited customer lock-in

- Dependency on foundational model companies

- Product risks where technology is moving so fast that these companies get disrupted themselves

Outcome

- Huge upside potential but with all the volatility

Examples

- Foundational model companies

- LLM wrappers

- AI-powered platforms, workflow and productivity tools

4. Transformable incumbents: Companies with the raw materials for AI-enabled reinvention

Characteristics

- Large install base and often deep integrations into enterprise systems

- Deep workflows and proprietary domain data accumulated over years

- Strong distribution, customer relationship and trust

Impact/Risk

- AI improves product stickiness, data improves AI quality

- Automation helps reduce costs and brings efficiency

- Can pivot to outcome based pricing

- AI can essentially be an amplifier for such companies turning them into intelligence platforms and improve earnings capabilities

Examples:

- Vertical SaaS platforms with deep domain data

- Industry-specific ERP systems

- Customer support platforms with massive ticket datasets

- Financial software with transaction history depth

- Healthcare workflow platforms with structured clinical data

Software is being sorted

Cloud changed distribution, but AI changes economics. AI is not just a feature upgrade. It is a prerequisite for economic survival. The companies that treat it as tooling will lag and the ones that treat it as architecture will compound.

The eventual winners will not be those who bolted AI onto old products, but those who re-engineer their products, pricing, and operations around AI as a structural advantage.

The Citrini piece is not a prophecy, but about how the market is beginning to think about AI’s impact and redrawing the software map. If there is a “SaaSpocalypse,” it will not be the end of software, but only the end of software that refuses to evolve.

The sorting has begun.

Interested in receiving more insights from Cover Drive Partners?

Subscribe below.